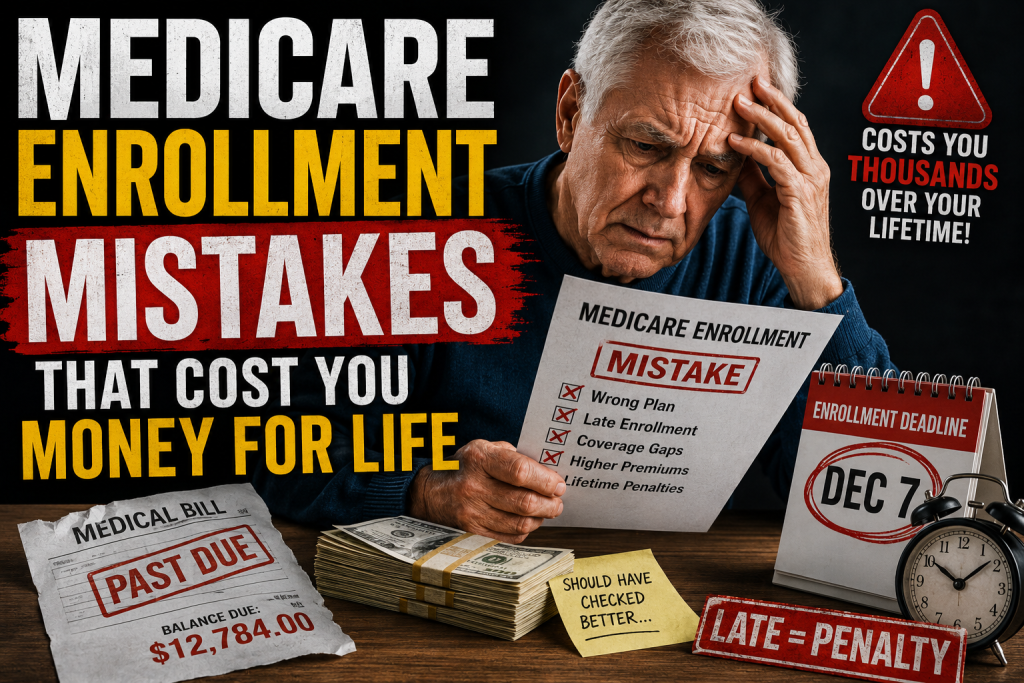

Most Medicare mistakes aren’t about choosing the wrong plan. They’re about missing a deadline, misunderstanding a rule, or making an assumption that turns out to be wrong.

And here’s the painful part: many of these mistakes are permanent. The federal government doesn’t have a “I didn’t know” exception. A penalty you incur at 65 can follow you for the rest of your life — adding hundreds or even thousands of dollars to your healthcare costs every single year.

After 18+ years of working exclusively in Medicare, I’ve seen every version of these mistakes. The retiree who thought COBRA would protect them. The couple who kept contributing to their HSA without realizing Medicare made those contributions illegal. The person who skipped Part D because they didn’t take any medications — and got hit with a penalty when they finally enrolled. If you’re new to Medicare overall, our Medicare for Dummies 2026 guide covers the full picture before diving into enrollment specifics.

None of these mistakes are hard to avoid. You just need to know the rules before you hit 65 — not after.

This guide covers the eight most costly Medicare enrollment mistakes people make, what they actually cost in real dollars, and exactly how to avoid every one of them.

Key Takeaways

- The Part B late enrollment penalty is 10% of your premium for every 12 months you delayed — permanently. At $202.90/month in 2026, two years of delay costs an extra $40.58 every month for life.

- COBRA does not count as creditable coverage for Medicare Part B. If you retire at 65, take COBRA, and skip Medicare enrollment, your penalty clock is already running.

- The Part D late enrollment penalty is 1% of the national base beneficiary premium ($38.99 in 2026) per uncovered month — permanently. Even if you take no medications, skipping Part D enrollment is a costly mistake.

- Your Medigap guaranteed issue window lasts only six months from your Part B effective date. Miss it and you may face medical underwriting — or be denied coverage entirely.

- If you have an HSA and delay Medicare enrollment past 65, Part A may be retroactively applied up to six months — making any HSA contributions during that period subject to a 6% IRS excise tax penalty.

- The marketplace coverage trap: if you have ACA marketplace coverage with subsidies, those subsidies end the moment you become eligible for premium-free Part A at 65 — whether you enroll or not.

- Working with an independent Medicare broker eliminates most of these risks. It costs you nothing and takes about 15 minutes.

Table of Contents

- Mistake #1: Missing Your Initial Enrollment Period

- Mistake #2: The COBRA Trap — The Most Expensive Misunderstanding in Medicare

- Mistake #3: Skipping Part D Because You Don’t Take Medications

- Mistake #4: Missing Your Medigap Guaranteed Issue Window

- Mistake #5: The HSA Trap — Contributing After Medicare Kicks In

- Mistake #6: Confusing Retiree Coverage for Creditable Coverage

- Mistake #7: The Marketplace Coverage Trap

- Mistake #8: Not Reviewing Your Plan Every Year

- What These Mistakes Actually Cost — In Real Dollars

- How to Protect Yourself

- Frequently Asked Questions

Mistake 1: Missing Your Initial Enrollment Period

Your Initial Enrollment Period (IEP) is the most important Medicare deadline you’ll ever face. It’s a 7-month window centered around your 65th birthday:

- 3 months before your birthday month

- Your birthday month

- 3 months after your birthday month

Miss this window without qualifying coverage elsewhere, and the consequences are both immediate and permanent.

What happens if you miss it:

You cannot enroll in Medicare Part B until the next General Enrollment Period (January 1 – March 31). Your coverage won’t start until July 1 of that year — leaving you potentially without medical coverage for months.

And then the penalty kicks in.

The Part B late enrollment penalty: For every full 12-month period you were eligible for Part B but didn’t enroll, your monthly premium increases by 10% — permanently. At the 2026 standard rate of $202.90/month:

- 1 year late: +$20.29/month → $223.19/month

- 2 years late: +$40.58/month → $243.50/month

- 3 years late: +$60.87/month → $263.77/month

That extra cost follows you every month for the rest of your life. Over a 20-year retirement, two years of delay can cost you nearly $10,000 in unnecessary premium payments — from one missed deadline. You can verify the current penalty structure directly at medicare.gov.

How to avoid it: Mark your IEP dates on your calendar the moment you turn 64. If you’re not receiving Social Security benefits, you’ll need to actively enroll at ssa.gov or at your local Social Security office. It won’t happen automatically.

Mistake 2: The COBRA Trap — The Most Expensive Misunderstanding in Medicare

This is the single most common — and most costly — Medicare enrollment mistake I see. And it happens to smart, well-prepared people all the time.

Here’s the scenario: You retire at 65. Your employer offers you COBRA coverage — the ability to continue your employer health plan for up to 18 months. You think: “Great. I have health insurance. I’ll hold off on Medicare until COBRA runs out.”

That reasoning is wrong. And it can cost you for life.

Why COBRA is a trap:

COBRA does not count as creditable coverage for Medicare Part B purposes. The moment your active employment ends, your 8-month Special Enrollment Period (SEP) clock starts ticking — regardless of whether you elect COBRA.

If you take COBRA and wait for it to run out before enrolling in Medicare, you will likely have missed your SEP entirely. At that point, you’ll have to wait for the next General Enrollment Period (January–March), your coverage won’t start until July, and you’ll owe a permanent Part B late enrollment penalty for every year you went without coverage.

A real example: You retire in June 2026. You elect 18 months of COBRA. Your SEP runs from June 2026 through January 2027 (8 months). If you don’t enroll in Medicare Part B by January 2027 — even though your COBRA coverage is still active — you’ve missed your window. You’ll wait until January 2028 for GEP, with July 2028 coverage — and owe a penalty for the entire time in between.

The important exception: Retiree drug coverage under COBRA may or may not be creditable for Part D purposes. Ask your COBRA plan administrator in writing whether your drug coverage is creditable for Medicare Part D. They are legally required to provide you with a “Notice of Creditable Coverage” annually. If it is creditable, you can delay Part D without penalty until COBRA ends.

How to avoid it: When you leave active employment, enroll in Medicare Parts A and B immediately. You can keep COBRA for dental, vision, or spouse coverage — but enroll in Medicare for your core medical coverage. Don’t let COBRA substitute for Medicare enrollment.

Mistake 3: Skipping Part D Because You Don't Take Medications

This one is counterintuitive — and it catches people off guard constantly.

You’re 65, healthy, and don’t take any prescription medications. So you figure: why pay for Part D drug coverage I don’t need?

Here’s why: the Medicare Part D late enrollment penalty is based on how long you go without creditable drug coverage — not on whether you actually needed the coverage.

How the penalty works:

The penalty is calculated as 1% of the national base beneficiary premium for every month you went without creditable drug coverage. In 2026, the national base beneficiary premium is $38.99, as confirmed by the National Council on Aging.

So: 1% × $38.99 × number of uncovered months = your monthly penalty — permanently.

Real dollar examples:

- 12 months without coverage: 12% × $38.99 = $4.70/month added permanently

- 24 months without coverage: 24% × $38.99 = $9.40/month added permanently

- 43 months without coverage: 43% × $38.99 = $16.80/month added permanently

These amounts seem small individually — but they compound. Over 20 years, 24 months of uninsured gap costs you over $2,200 in extra premiums. And since the penalty recalculates annually based on the current base premium — which tends to rise — the actual lifetime cost grows over time.

The bigger risk:

If you develop a health condition at 70 and suddenly need expensive medications, you’ll pay full price until the next enrollment period — and then pay the penalty on top of your premium for the rest of your life.

How to avoid it: Always enroll in a Part D plan when you first become eligible — even if it’s the lowest-cost plan available in your area. The protection is worth far more than the premium.

Mistake 4: Missing Your Medigap Guaranteed Issue Window

This is the mistake that most agents don’t explain clearly enough — and that has the longest-lasting consequences.

When you first enroll in Medicare Part B, you have a 6-month Medigap Open Enrollment window — starting the first day your Part B coverage is effective. During this window, every insurance company selling Medigap plans in your state must:

- Accept your application

- Charge you the standard rate for your age

- Cover you regardless of your health history

No health questions. No underwriting. No denials.

This window is guaranteed by federal law. And it only comes around once.

What happens when you miss it:

Outside of this window and specific state-protected situations, Medigap insurers can — and often do — ask health questions and deny your application based on your medical history. The older you get and the more health conditions you develop, the harder it becomes to qualify for a Medigap plan.

In most states, once you’re past your guaranteed issue window without a qualifying event, you may be unable to get a Medigap plan at all if you have significant health conditions.

The 12-month trial right:

There is one important protected window many people don’t know about: if you enroll in a Medicare Advantage plan for the first time at 65 and decide within the first 12 months that it’s not right for you, you have a guaranteed right to switch to any Medigap plan — without underwriting. This trial right exists only once, at your first enrollment.

New York exception:

If you live in New York, you have year-round guaranteed issue — you can apply for Medigap at any time without underwriting, regardless of health status. This is an exceptional consumer protection that most states don’t offer.

How to avoid it:

Enroll in your Medigap plan during your 6-month guaranteed issue window. Don’t wait until you’re sick to think about supplemental coverage — by then, it may be too late to qualify. When you’re ready to choose a carrier, our guide on how to check a Medicare Supplement company’s financial strength will help you pick the right one.

Mistake 5: The HSA Trap — Contributing After Medicare Kicks In

This one surprises almost everyone — and it carries an IRS tax penalty on top of a Medicare compliance issue.

If you have a Health Savings Account (HSA) and are still contributing to it, you need to stop making contributions before you enroll in Medicare. Here’s why.

The rule: Once you’re enrolled in any part of Medicare — including Part A — you are no longer eligible to contribute to an HSA. Any contributions made after your Medicare enrollment are considered “excess contributions” by the IRS, subject to a 6% excise tax penalty for every year the excess remains in the account.

The retroactive trap:

Here’s where it gets tricky. When you enroll in Medicare Part A after age 65, your coverage can be applied retroactively for up to six months — but never before your 65th birthday.

This means if you enroll in Medicare in October and your Part A is retroactively applied to April, any HSA contributions you made from April through September are now excess contributions — even though you didn’t know you were technically enrolled yet.

A real example: You’re 67 and plan to retire in June 2026. In January 2026, you fully fund your HSA ($4,400 for 2026). When you enroll in Medicare in June 2026, Part A is retroactively applied to December 2025. Your entire 2026 HSA contribution is now excess — and subject to a 6% annual penalty until corrected.

How to avoid it:

Stop making HSA contributions at least 6 months before you plan to enroll in Medicare or apply for Social Security benefits (which triggers automatic Part A enrollment). Mark this date on your calendar well in advance.

If you accidentally contribute after your Medicare enrollment begins, work with your HSA administrator promptly to withdraw the excess amount and any earnings before your tax filing deadline to minimize the penalty.

Mistake 6: Confusing Retiree Coverage for Creditable Coverage

Many people leave their job with retiree health benefits — coverage their former employer provides in retirement. They assume this coverage protects them from Medicare enrollment penalties the same way active employer coverage does.

Often, it doesn’t.

The distinction:

Active employer coverage — health insurance tied to current employment at a company with 20+ employees — qualifies you for a Special Enrollment Period and protects you from Part B penalties.

Retiree health coverage — insurance provided by a former employer after you’ve stopped working — is generally not considered active employer coverage for Medicare purposes. In most cases, you should enroll in Medicare at 65 even if you have retiree benefits, because Medicare typically becomes your primary insurance.

What to ask before assuming:

Contact your former employer’s HR or benefits department and ask two specific questions:

- “Is my retiree health coverage considered creditable for Medicare Part B?”

- “Is my retiree prescription drug coverage considered creditable for Medicare Part D?”

Get the answers in writing. Keep the documentation. The answers will determine whether you need to enroll at 65 or whether you have more flexibility.

The important nuance:

Some employer retiree plans are specifically designed to wrap around Medicare — meaning they expect you to have Medicare as primary coverage and pay second. Enrolling in Medicare actually activates the full value of these plans. Not enrolling can leave you with unexpected gaps and penalties.

Mistake 7: The Marketplace Coverage Trap

If you purchased health coverage through the ACA marketplace (Healthcare.gov) and you’re receiving premium tax credits (subsidies), there’s something critically important to understand as you approach 65.

The rule:

The moment you become eligible for premium-free Medicare Part A — which happens automatically when you turn 65 if you have 40+ work quarters — you are no longer eligible for marketplace premium tax credits, even if you haven’t yet enrolled in Medicare.

This catches people completely off guard. Your subsidy eligibility ends whether or not you’ve actually signed up for Medicare. If you continue receiving subsidies after your Part A eligibility begins, you may owe them back at tax time.

What to do:

As you approach 65, contact your marketplace plan and notify them of your Medicare eligibility. Enroll in Medicare during your IEP to ensure seamless coverage and avoid any subsidy repayment issues.

Mistake 8: Not Reviewing Your Plan Every Year

This mistake is less about enrollment and more about complacency — and it costs people real money every year.

Medicare plans change annually. Premiums go up. Drug formularies change. Doctors leave networks. Benefits that existed this year disappear next year.

The Annual Enrollment Period (AEP) — October 15 through December 7 — exists specifically so you can review your coverage and make changes for the coming year. Every Medicare beneficiary should be doing this review every single year, not just when they first enroll.

What to review each AEP:

- Part D: Check whether your current medications are still covered at the same tier. Compare your current plan to alternatives using Medicare’s Plan Finder at medicare.gov/plan-compare.

- Medicare Advantage: Read your Annual Notice of Change (ANOC), mailed in late September. Check whether your doctors are still in-network, whether your drug coverage has changed, and whether the premium and out-of-pocket maximum have shifted.

- Medigap: Compare your current premium against what comparable A-rated carriers are offering. If your rate has increased significantly, it may be worth exploring alternatives — especially if you’re still in good health.

One thing most people don’t do:

If you’re on a Medigap plan, compare the rate increase you received this year against what other carriers are charging for the same plan. Rate increases vary significantly by carrier. If your carrier raised rates 18% and a comparable A-rated carrier is offering the same Plan G for 25% less, that’s real money worth acting on — while you can still qualify medically.

What These Mistakes Actually Cost — In Real Dollars

Let’s put this all together with actual numbers so the stakes are clear:

|

Mistake |

Annual Cost |

Lifetime Cost (20 years) |

|---|---|---|

|

Part B penalty — 1 year late |

+$243/year |

+$4,860 |

|

Part B penalty — 2 years late |

+$487/year |

+$9,740 |

|

Part B penalty — 3 years late |

+$730/year |

+$14,600 |

|

Part D penalty — 24 months uncovered |

+$113/year |

+$2,260+ |

|

Part D penalty — 43 months uncovered |

+$202/year |

+$4,040+ |

|

HSA excess contribution (6% IRS penalty) |

6% of excess per year until corrected |

Varies |

|

Medigap missed window (uninsurable) |

Cost of uncovered care |

Potentially unlimited |

How to Protect Yourself

The single most effective thing you can do to avoid every mistake on this list is to start planning 6 to 9 months before your 65th birthday — not 6 weeks.

Your pre-65 checklist:

☐ Confirm your IEP dates (3 months before your birthday month)

☐ If you have employer coverage, confirm in writing whether it’s creditable for Part B and Part D

☐ If you have COBRA or retiree coverage, confirm exactly how Medicare interacts with it — don’t assume

☐ If you have an HSA, stop contributions at least 6 months before enrolling in Medicare or applying for Social Security

☐ If you have ACA marketplace coverage with subsidies, notify your marketplace plan of your upcoming Medicare eligibility

☐ Enroll in Medicare Parts A and B during your IEP

☐ Enroll in a Medigap plan during your 6-month guaranteed issue window

☐ Enroll in a Part D plan even if you don’t take medications

☐ Set a calendar reminder every October 15 for your annual plan review

Work with an independent Medicare broker. A Medicare-only broker who represents 40+ carriers will walk you through every one of these decisions, confirm your specific situation, and make sure you don’t miss a deadline or make a costly assumption. It costs you nothing — brokers are compensated by the carriers when you enroll, and your premium is the same regardless.

Frequently Asked Questions

Note: Part D penalty amounts recalculate annually based on the base beneficiary premium, which typically increases over time — meaning lifetime costs grow.

You’ll likely have to wait until the General Enrollment Period (January 1 – March 31) to enroll in Part B, with coverage starting July 1. You’ll also face a permanent Part B late enrollment penalty of 10% for every full 12-month period you delayed. The gap in coverage and the permanent premium increase make missing your IEP one of the most costly Medicare mistakes possible.

No — not for Part B. COBRA does not protect you from the Part B late enrollment penalty. Your 8-month Special Enrollment Period starts when your active employment ends, regardless of whether you elect COBRA. However, COBRA drug coverage may or may not be creditable for Part D — you must get written confirmation from your plan administrator to know for sure.

The penalty is 10% of the standard Part B premium for every full 12-month period you were eligible but didn’t enroll. In 2026, the standard Part B premium is $202.90/month. One year late means an extra $20.29/month — permanently. Two years late means an extra $40.58/month — permanently.

The penalty is 1% of the national base beneficiary premium ($38.99 in 2026) for every month you went without creditable drug coverage. The monthly penalty is rounded to the nearest $0.10 and added to your Part D premium permanently. For 24 months without coverage, that’s approximately $9.36 added to your monthly premium for life.

Stop making HSA contributions at least 6 months before you plan to enroll in Medicare or apply for Social Security benefits. This is because Medicare Part A can be applied retroactively for up to 6 months after enrollment. Any contributions made during retroactive Medicare months are considered excess contributions subject to a 6% IRS excise tax penalty annually until corrected.

It’s the 6-month period starting on the date your Medicare Part B becomes effective. During this window, every Medigap insurer must accept your application at standard rates without health questions or medical underwriting. This window comes around once — missing it can mean being denied Medigap coverage entirely if you develop health conditions.

In most states, you can apply at any time — but outside of protected windows, the insurer can ask health questions and may decline your application. New York is an exception — it offers year-round guaranteed issue, meaning you can switch or enroll at any time without underwriting. A handful of other states have birthday rules or similar protections that create annual windows.

If your employer has 20 or more employees and you’re covered under active employer health insurance, you can delay Medicare enrollment without penalty. Once that coverage ends, you have 8 months to enroll under a Special Enrollment Period. Keep documentation of your employer coverage in case Social Security asks for proof.

Generally no. Retiree health coverage from a former employer typically does not qualify as creditable coverage for avoiding the Part B penalty the way active employer coverage does. You should enroll in Medicare at 65 even if you have retiree benefits, and confirm with your plan how Medicare coordinates with your retiree coverage.

Medicare penalties are permanent. Medicare deadlines are firm. And the assumptions that seem reasonable — COBRA will protect me, I don’t need drug coverage yet, my retiree plan handles everything — are the exact assumptions that lead to the most expensive mistakes.

The good news: every mistake in this guide is entirely avoidable with the right information at the right time. That’s why starting your Medicare planning 6 to 9 months before your 65th birthday — not 6 weeks — makes such a meaningful difference.

Medicare foundation, our guide on what Medicare actually covers and what it doesn’t is a great next read. A 15-minute conversation can protect you from a lifetime of unnecessary expenses.

Paul Barrett is the founder and Principal Agent of The Modern Medicare Agency, a Medicare-only independent brokerage based in Melville, NY. With 18+ years of Medicare-exclusive experience, licensure in 34 states, and relationships with 40+ carriers, Paul has helped 5,000+ clients navigate Medicare with clarity and confidence. He is the author of Medicare Mastery Unlocked.

If you’d like to walk through your specific situation — your employer coverage, your HSA, your timeline, your plan options — I’m happy to do that at no cost. And if you’re still building your